Author: Dr. William J Lossef, DDS | VP of Practice Transitions

Wondering How Your Payer Mix Affects Practice Value?

Get a free valuation that models PPO write offs, DHMO capitation, and what buyers will actually pay for your collections.

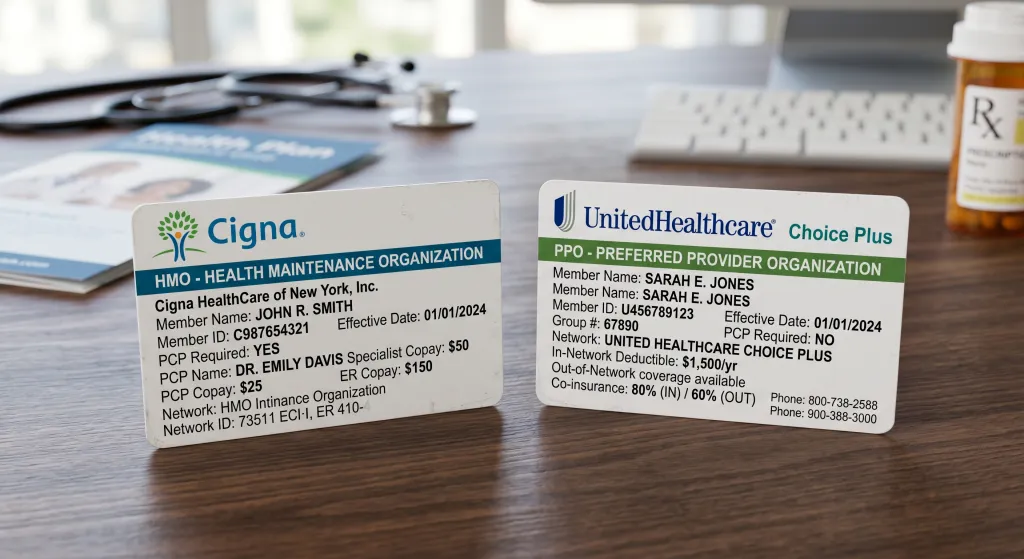

Get a Free ValuationAn HMO dental plan locks you into a small network of dentists in exchange for low or zero out of pocket costs on most cleanings and fillings. A PPO plan costs more each month but lets you visit any licensed dentist, with the largest savings when you stay in network. Roughly four out of five privately insured Americans hold a PPO style dental plan, which is why most US practices accept PPO insurance.

The choice between HMO and PPO dental coverage shapes what you pay at the front desk, how much paperwork you handle, and whether you can keep the family dentist you already trust. The decision matters just as much on the other side of the operatory. Practice owners who accept the wrong mix of plans watch their collections erode one write off at a time. This guide covers both angles, so patients pick a plan that fits their life and owners build a payer mix that fits their financial goals.

HMO vs PPO Dental Plans at a Glance

Here is the side by side breakdown across the 12 dimensions that actually move the needle for patients and practices.

| Feature | HMO (DHMO) | PPO (DPPO) |

|---|---|---|

| Network restriction | Must use assigned in network dentist | Any licensed dentist, best rates in network |

| Monthly premium | Lower, often under 20 dollars solo | Higher, often 30 to 60 dollars solo |

| Annual deductible | Usually none | 50 to 100 dollars per person |

| Annual maximum | No cap on most services | 1,000 to 2,500 dollars typical |

| Out of pocket cost | Fixed copay per service | Coinsurance after deductible |

| Choice of dentist | Limited to plan roster | Open, with cost penalty out of network |

| Specialist referrals | Required from primary dentist | Not required |

| Claims paperwork | Minimal, dentist handles billing | Standard claim forms, sometimes patient filed |

| Waiting periods | Rare | Common for major and orthodontic work |

| Balance billing | Not allowed in network | Allowed out of network |

| Coverage outside network | None, emergencies only | Reduced reimbursement, still covered |

| Dentist payment model | Capitation, per member per month | Discounted fee for service |

The table tells the story in one glance. HMO plans win on price and simplicity. PPO plans win on flexibility and dentist choice. Everything else in this guide is a deeper look at the trade offs hidden inside those two columns.

If you only remember one rule of thumb, make it this. An HMO is a budget tool with guardrails. A PPO is a flexibility tool with a higher sticker price. Neither is universally better. The right answer depends on who your dentist is, what work you need, and how much paperwork you tolerate.

What Is an HMO Dental Plan

An HMO dental plan, more accurately called a DHMO (Dental Health Maintenance Organization), works on a capitation model. The insurer pays a fixed monthly amount to a contracted dentist for every member assigned to that office, whether the patient walks through the door or not. In exchange, the dentist agrees to provide a defined list of services at zero cost or a small flat copay.

That structure is why DHMOs are cheap. There is no claim cycle, no fee negotiation per visit, and no surprise denials. Patients pick a primary dentist from the network roster at enrollment and stick with that office for routine care. If they need a specialist like an endodontist or oral surgeon, the primary dentist writes a referral.

DHMOs suit people who want predictable monthly costs, do not have a longtime dentist they refuse to leave, and mostly need cleanings, fillings, and the occasional crown. They are common in California, Texas, and Florida where employers buy them as a low premium option alongside PPO plans.

How DHMO Plans Pay Dentists

The capitation model is the reason fewer practices accept DHMOs. A dentist might receive 8 to 15 dollars per member per month for an assigned patient panel. If a patient comes in twice a year for cleanings and one filling, the math can work. If that same patient needs a root canal, a crown, and periodontal therapy, the practice loses money on every appointment.

Practices that accept DHMOs do so for one reason. Volume. A guaranteed monthly check for hundreds of assigned members creates a baseline of revenue and fills the schedule with patients who would otherwise not come in at all. Owner operators with excess chair capacity and a strong hygiene program can make capitation work. Specialty practices and fee for service offices rarely participate.

What Is a PPO Dental Plan

A PPO (Preferred Provider Organization) dental plan contracts with a network of dentists who agree to discounted fees in exchange for patient referrals from the insurer. Patients can visit any licensed dentist in the country, but they pay less when they choose a contracted in network provider. Out of network visits are still covered, just at a lower reimbursement rate.

PPO plans dominate the US dental market. They give patients the freedom to keep a longtime dentist, see a specialist without a referral, and travel without losing coverage. The trade off is a higher monthly premium, an annual deductible, and an annual maximum benefit that usually caps somewhere between 1,000 and 2,500 dollars.

The coverage structure is tiered. Preventive care like cleanings and exams is typically covered at 100 percent in network. Basic work like fillings runs around 80 percent coinsurance. Major work like crowns, bridges, and implants sits at 50 percent, often after a waiting period of six to twelve months. Orthodontia, when included, has its own lifetime maximum.

How PPO Fee Schedules Work for Practice Owners

Every PPO contract a practice signs comes with a fee schedule. That schedule tells the dentist what each insurer will pay for each procedure, regardless of what the office bills. The gap between the practice's usual customary and reasonable (UCR) fee and the PPO contracted fee is the write off. Across most US markets, PPO write offs run 25 to 45 percent.

That is the core tension of PPO participation. Signing more contracts fills the schedule and stabilizes new patient flow. Each contract also reduces the per visit revenue on every procedure performed for those members. Some practices participate with two or three top PPOs to access the largest patient pools. Others go fully out of network and rely on reputation, marketing, and a smaller volume of higher revenue patients.

DHMO vs PPO. The Practical Differences for Patients

The decision usually comes down to four questions. How much do you want to pay each month, how attached are you to a specific dentist, how much dental work do you anticipate, and how do you feel about paperwork.

- Pick a DHMO if. You want the lowest monthly premium, you do not have a current dentist or you are willing to switch, you mostly need preventive care and basic fillings, and you live in a metro area with a strong DHMO network.

- Pick a PPO if. You already love your dentist and want to keep going, you anticipate major work like crowns or implants, you travel frequently and need coverage outside your home market, or you want the option to see a specialist without a referral.

- Pick a DHMO if. You are a young single adult on a tight budget who has not had a cavity in years and just needs cleanings.

- Pick a PPO if. You have a family with kids approaching orthodontic age and you want flexibility on which orthodontist to choose.

- Pick a DHMO if. You want to skip the claim forms and never see a bill beyond the copay at checkout.

What About DMO and DPPO

The alphabet soup of dental plan acronyms confuses almost everyone. Here is the short version. DMO stands for Dental Maintenance Organization and is functionally the same as a DHMO. Aetna popularized the DMO label, while most other carriers use DHMO. Same structure, same restrictions, different marketing.

DPPO is just the dental version of PPO. When you see DPPO in an insurance brochure, it means Dental Preferred Provider Organization. The rules are identical to a medical PPO transplanted into the dental world.

Two other plan types round out the market. Indemnity plans (sometimes called fee for service plans) pay a fixed percentage of any dentist's billed fee with no network at all. They are rare today and usually expensive. Discount dental plans are not insurance. They are membership programs that give you a price break at participating offices in exchange for an annual fee. They can be useful for uninsured adults who need predictable savings on routine care.

Delta Dental PPO vs Delta Dental Premier

Delta Dental runs the largest dental network in the country, and the company sells two different PPO style products that confuse many patients. Delta Dental PPO and Delta Dental Premier sound similar but pay dentists very differently.

| Feature | Delta Dental PPO | Delta Dental Premier |

|---|---|---|

| Network size | Smaller, more selective | Largest in the country |

| Dentist discount | Larger write offs (often 25 to 40 percent) | Smaller write offs (often 10 to 25 percent) |

| Patient out of pocket | Lowest in network cost | Higher than PPO, lower than out of network |

| Monthly premium | Higher | Lower |

| Practice participation | Selective, fewer dentists opt in | Broad, most general dentists participate |

The practical takeaway for patients is that a Delta Dental PPO plan saves more per visit, but only if your dentist is a contracted PPO provider. Premier is the larger network, so if your dentist takes "Delta Dental" it is more likely they are a Premier provider than a PPO provider. Always verify the specific plan tier when you call the office.

For practice owners, the decision to contract with Delta PPO is one of the most consequential payer choices you make. Premier participation comes with a smaller write off but limits the discount Delta can advertise to patients. PPO participation generates more steering from Delta but cuts deeper into per procedure revenue. Many practices participate in Premier only, keeping Delta volume without the steepest PPO discount.

What This Means If You Own a Dental Practice

Insurance participation is the single biggest lever an owner controls outside of clinical productivity. The contracting decision sets a floor on your collection rate, shapes your new patient flow, and defines the operational complexity of your billing department.

The math is straightforward and brutal. If your UCR fee for a crown is 1,400 dollars and the PPO contracted rate is 900 dollars, every contracted crown you place is a 500 dollar write off. Across a year and a thousand procedures, those write offs add up to the difference between a practice that pays the owner well and a practice that grinds along on volume.

The right payer mix depends on the practice. A startup or fast growing practice with empty chairs benefits from PPO contracts that fill the schedule. A mature practice with a full hygiene book and an established patient base can drop the worst paying contracts and accept the new patient slowdown in exchange for higher per visit revenue. A specialty practice typically participates in fewer plans because the patient referral pattern works differently.

When you eventually sell, buyers look hard at your payer mix. A practice running 80 percent on the lowest paying DHMO and PPO contracts in the market sells at a different multiple than a practice with 40 percent fee for service and a balanced PPO panel. The decisions you make today on which plans to accept directly shape the value buyers assign three or five years from now. Our team builds detailed payer mix analyses inside every dental practice valuation, because what is on the schedule today drives what the practice is worth tomorrow.

How to Pick the Right Dental Insurance Plan

If you are choosing between an HMO and PPO offer from your employer or on the individual market, run through this checklist before you enroll.

- Confirm your current dentist is in network. Call the office and ask which specific plan tiers they participate in. A dentist who takes "Delta Dental" may not take Delta PPO.

- Check waiting periods for major work. If you need a crown or implant in the next twelve months, look for a plan with no waiting period or a credit for prior coverage.

- Compare annual maximums. A 1,000 dollar maximum disappears fast if you need root canal therapy. A 2,000 or 2,500 dollar maximum is worth a higher monthly premium for many adults.

- Look at the orthodontia rider. If you have kids, the lifetime ortho maximum and waiting period matter more than the routine coverage. Some plans exclude orthodontia entirely.

- Add up the true annual cost. Premium plus deductible plus expected copays beats comparing premium alone. A 15 dollar a month DHMO can cost more than a 45 dollar PPO once you need a crown.

- Read the missing tooth clause. Many plans refuse to cover replacement of a tooth lost before the policy started. This single clause sinks more implant claims than any other.

Common Questions About HMO and PPO Dental Plans

Is HMO or PPO Better for Dental

Neither is universally better. HMO plans cost less and remove paperwork but force you into a small network. PPO plans cost more but let you keep any dentist and see specialists without a referral. If budget is your top priority and you do not have a current dentist, an HMO usually wins. If flexibility matters or you anticipate major work, a PPO usually wins.

Can You Go to Any Dentist With a PPO Plan

Yes. A PPO plan covers any licensed dentist in the country. You pay the least when you visit a contracted in network provider, more when you visit an out of network dentist, and any difference between the billed fee and the insurer's allowed amount may come out of your pocket.

Do HMO Dental Plans Cover Orthodontics

Some do, some do not, and the ones that do usually cover only children. When orthodontia is included on an HMO, it appears as a flat copay schedule, often around 1,800 to 2,500 dollars for full comprehensive treatment. Adult orthodontia is rarely covered. Always check the specific plan documents, since orthodontic riders vary heavily even within the same carrier.

What Is the Difference Between Dental HMO and Dental PPO

A DHMO assigns you to one primary dentist, pays that dentist a fixed monthly capitation amount, and gives you zero or low copays on a defined service list. A DPPO contracts with a network of dentists at discounted fee schedules, lets you visit any of them or any out of network dentist, and pays a percentage of the cost after a deductible.

Are HMO Dental Plans Worth It

HMO plans are worth it for adults and families who want the lowest monthly premium, mostly need preventive and basic care, do not have a strong attachment to a specific dentist, and live in an area with a robust DHMO network. They are not worth it for people who want to keep an existing dentist who is not in the HMO network, anticipate major or specialty work, or value the option to switch providers easily.

What Happens if I See an Out of Network Dentist With a PPO

You can still see them, the visit is still covered, and you will pay more than you would in network. The insurer reimburses based on its own allowed amount rather than the dentist's billed fee. The dentist can balance bill you for the difference, the deductible may be higher, and the coinsurance percentage often shifts in the insurer's favor. Some plans also use separate annual maximums for in network and out of network care.

Whether you are picking a plan for your family or building the payer mix that drives your practice's collections, the contracting decisions in front of you compound for years. Practice owners thinking about an eventual exit should understand exactly how their PPO and DHMO participation shapes valuation before they sit down with a buyer. Our team has helped hundreds of dentists model the trade off and prepare for sale, starting with a confidential practice valuation. When you are ready to take the next step, reach out about our sell a dental practice process and we will walk you through the numbers your future buyer will care about most.